Under the terms of the Transaction, Anfield shareholders will receive 0.031 of a common share of IsoEnergy (each whole share, an “ISO Share”) for each Anfield Share held (the “Exchange Ratio”). Existing shareholders of IsoEnergy and Anfield will own approximately 83.8% and 16.2% on a fully-diluted in the-money basis, respectively, of the outstanding ISO Shares on closing of the Transaction.

The Exchange Ratio implies consideration of $0.103 per Anfield Share, based on the closing price of the ISO Shares over all Canadian exchanges on October 1, 2024. Based on each company’s 20-day volume weighted average trading price over all Canadian exchanges for the period ending October 1, 2024, the Exchange Ratio implies a premium of 32.1% to the Anfield Share price. The implied fully-diluted in the-money equity value of the Transaction is equal to approximately $126.8 million.

Strategic Rationale

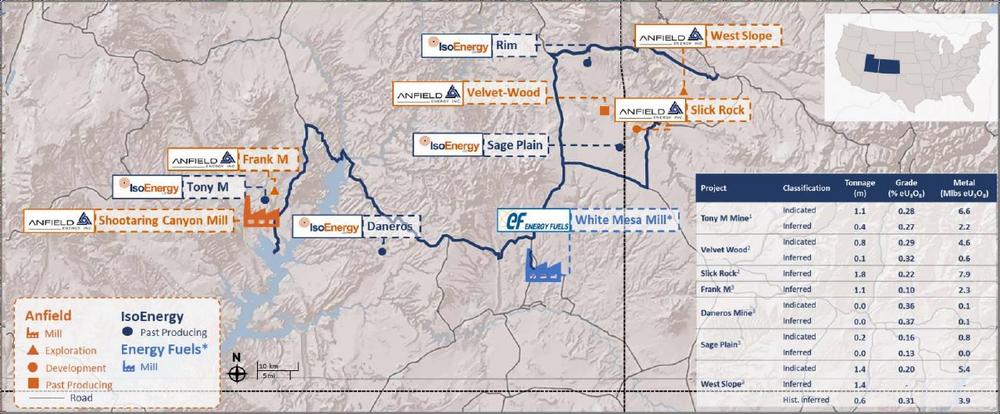

- Expected to Expand Near-Term U.S. Uranium Production Capacity – The combined portfolio (“Combined Portfolio”) of permitted past-producing mines and development projects in the Western U.S. (Figure 1) is expected to provide for substantial increased uranium production potential in the short, medium and long term.

- Ownership of Shootaring Canyon Mill Secures Access to Two of Only Three U.S. Permitted Conventional Uranium Mills –

– A restart application has been submitted to the State of Utah for the Shootaring Canyon Mill to increase throughput from 750 stpd to 1,000 stpd and expand licensed annual production capacity from 1 million lbs U₃O₈ to 3 million lbs U₃O₈.

– Existing toll-milling agreements with Energy Fuels at the White Mesa Mill provide additional processing flexibility for current IsoEnergy mines.

- Meaningful Growth in U.S. Uranium Mineral Endowment – With combined current mineral resources of 17.0 Mlbs Measured & Indicated (+157%) and 10.6 Mlbs Inferred (+382%)[1], and historical mineral resources of 152.0 Mlbs Measured & Indicated (+14%), and 40.4 Mlbs Inferred[2] (+33%), the proforma company will rank among the largest in the U.S.

- Complementary Project Portfolio Provides Immediate Operational Synergies – Benefits from the proximity of the Combined Portfolio in Utah and Colorado are expected to include, reduced transportation costs, increased operational flexibility for mining and processing, reduction in G&A on a per lb basis, and risk diversification through multiple production sources.

- Aligned with Goal of Building a Multi-Asset Uranium Producer in Tier-One Jurisdictions – Beyond the impressive Combined Portfolio in the U.S., the proforma company will have a robust pipeline of development and exploration-stage projects in tier-one uranium jurisdictions, including the world’s highest grade published Indicated uranium resource in Canada’s Athabasca Basin.

- Well-Timed to Capitalize on Strong Momentum in the Nuclear Industry – Recent industry headlines relating to increasing demand and support for nuclear power are expected to drive uranium demand and by extension prices, coinciding with expected production and development of the Combined Portfolio.

CEO and Director of IsoEnergy, Philip Williams, commented, “IsoEnergy is committed to becoming a globally significant, multi-asset uranium producer in the world’s top uranium mining jurisdictions. The U.S. is a key jurisdiction for us, and we believe today’s acquisition of Anfield strengthens both our resource base and near-term production potential. The combined uranium mineral endowment will rank as one of the largest in the U.S., supported by a 100% owned processing facility, multiple fully permitted mines ready for rapid restart, and a strong pipeline of longer-term development projects.

With the global shift towards nuclear power, we believe the outlook for uranium has never been stronger, making this a pivotal move for IsoEnergy at the right time. We commend the Anfield team for assembling and managing this impressive portfolio over the years, and we look forward to advancing these assets back into production into a time of anticipated rising demand for uranium.”

CEO and Director of Anfield, Corey Dias, commented, “We believe this Transaction represents an excellent opportunity for Anfield shareholders, and the culmination of our team’s strategic approach to assembling a unique, U.S.-focused portfolio of potential near-term uranium production assets. This Transaction underscores our view that Anfield acquired the right assets in the right place at the right time.”

“Beyond the immediate share price premium, shareholders will gain exposure to a broad array of uranium projects, from the high grade and strategically located Hurricane project in Saskatchewan to a large inventory of earlier stage resource assets. The most fundamental benefit of the Transaction is the high level of economic synergies that we believe will be generated by the marriage of our mill and mining assets with IsoEnergy’s U.S. mining assets, particularly the advanced stage Tony M mine which is located within 4 miles of our Shootaring Canyon mill. Other tangential benefits to Anfield shareholders will include higher levels of trading liquidity, a robust combined balance sheet, and exposure to extensive research analyst coverage and institutional ownership. We look forward to working with the IsoEnergy team to complete the Transaction and to integrating our two platforms with a view to revitalize American uranium mining in pursuit of clean, domestic energy security.”

Benefits to IsoEnergy Shareholders

- Secures Shootaring Canyon Mill, one of only three permitted conventional uranium mills in the U.S., located adjacent to IsoEnergy’s Tony M Mine

- Diversified access to both Shootaring Canyon and White Mesa Mills to boost near-term production capacity while unlocking anticipated operational synergies

- Strengthens ranking among the U.S. uranium players in terms of production capacity, advanced mining assets and resource exposure

- Potential re-rating from de-risking near-term potential production, increased scale, asset diversification within the U.S. and additional exploration upside

- A combined company backed by corporate and institutional investors of Anfield including, enCore Energy Corp.

- Creation of a larger platform with greater scale for M&A, access to capital and liquidity

Benefits to Anfield Shareholders

- Immediate and attractive premium

- Exposure to a larger, more diversified portfolio of high-quality uranium exploration, development and near-term production assets in tier one jurisdictions of U.S., Canada and Australia

- Entry into the Athabasca Basin, a leading uranium jurisdiction, with the high-grade Hurricane deposit

- Upside from an accelerated path to potential production as well as from synergies with IsoEnergy’s other Utah uranium assets

- A combined company backed by corporate and institutional investors of IsoEnergy including, NexGen Energy Ltd., Energy Fuels Inc., Mega Uranium Ltd. and uranium ETFs

- Participation in a larger platform with greater scale for M&A

- Increased scale expected to provide greater access to capital, trading liquidity and research coverage

Shootaring Canyon Mill and Velvet-Wood and Slick Rock Uranium Projects

Located approximately 48 miles (77 kilometers) south of Hanksville, Utah and 4 miles from IsoEnergy’s Tony M Mine, the Shootaring Canyon Mill is one of three licensed, permitted and constructed conventional uranium mills in the United States. Built in 1980 by Plateau Resources, the mill commenced operations in 1982 but ceased operations due to the decline in the uranium price after approximately six months of operation. Despite its relatively short period of operation, the Mill historically produced and sold 27,825 lbs of U3O8. The Mill has not been decommissioned and has been under care and maintenance since cessation of operations. The Shootaring Canyon Mill has a radioactive source materials license on Standby status which will need to be amended, among other things, to allow Mill operations to resume.

In May 2023, Anfield completed a Preliminary Economic Assessment assuming that mineral processing of the Velvet-Wood and Slick Rock Projects would take place at the Shootaring Canyon Mill.

The Velvet-Wood project is a 2,425-acre property located in the Lisbon Valley uranium district of San Juan County, Utah, which was previously the largest uranium producing district in Utah. The Velvet-Wood Uranium project consists of two areas with mineral resources as outlined below.

Past production from underground mines in the Velvet area during 1979 to 1984 yielded significant results, recovering around 4 Mlbs of U3O8 and 5 Mlbs of V2O5 from mining approximately 400,000 tons of ore with grades of 0.46% U3O8 and 0.64% V2O5. The Velvet mine retains underground infrastructure, including a 3,500 ft long, 12′ x 9′ decline to the uranium deposit. Along with the Tony M Mine, the Velvet-Wood Project is the most advanced uranium asset in the Combined Portfolio and is believed to represent a potential near-term path to uranium and vanadium production.

The Slick Rock property is an advanced stage conventional uranium and vanadium project located in San Miguel County, Colorado. The project consists of 315 contiguous mineral lode claims and covers approximately 5,333 acres. Past production came from the upper or third-rim sandstone of the Salt Wash member of the Morrison Formation. This is the target host for uranium/vanadium mineralization within Anfield’s Slick Rock project area.

Board of Directors’ Recommendations

The Arrangement Agreement has been unanimously approved at meetings of the board of directors of each of IsoEnergy and Anfield, including, in the case of Anfield, following, among other things, the receipt of the unanimous recommendation of a special committee of independent directors of Anfield. Evans & Evans, Inc. provided an opinion to the special committee of Anfield and Haywood Securities Inc. provided an opinion to the board of directors of Anfield, to the effect that, as of the date of such opinion, the consideration to be received by Anfield shareholders pursuant to the Transaction is fair, from a financial point of view, to the Anfield shareholders, subject to the limitations, qualifications and assumptions set forth in such opinion. The board of directors of Anfield unanimously recommends that Anfield securityholders vote in favour of the Transaction. Canaccord Genuity Corp. provided an opinion to the board of directors of IsoEnergy to the effect that, as of the date of such opinion, the consideration to be paid to Anfield shareholders pursuant to the Transaction is fair, from a financial point of view, to IsoEnergy, subject to the limitations, qualifications and assumptions set forth in such opinion. The board of directors of IsoEnergy unanimously recommends that IsoEnergy shareholders vote in favour of the Transaction.

Material Conditions to Completion of the Transaction

The Transaction will be effected by way of a court-approved plan of arrangement under the Business Corporations Act (British Columbia), requiring the approval of (i) at least 662/3% of the votes cast by Anfield shareholders, (ii) if required, a simple majority of the votes cast by Anfield shareholders, excluding certain related parties as prescribed by Multilateral Instrument 61-101 – Protection of Minority Security Holders in Special Transactions, voting in person or represented by proxy at a special meeting of Anfield shareholders to consider the Transaction (the “Anfield Meeting”); and (iii) a simple majority of votes cast by shareholders of IsoEnergy, voting in person or represented by proxy at a special meeting of IsoEnergy shareholders to consider the Transaction (the “IsoEnergy Meeting”) or by written resolution. The Anfield Meeting and the IsoEnergy Meeting, if applicable, are expected to take place in November 2024. An information circular regarding the Transaction will be filed with regulatory authorities and mailed to Anfield shareholders and, if applicable, to IsoEnergy shareholders, in accordance with applicable securities laws. The Transaction is expected to be completed in the fourth quarter of 2024, subject to satisfaction of the conditions under the Arrangement Agreement.

Each of Anfield’s and IsoEnergy’s directors and officers, along with certain key shareholders, including enCore Energy Corp., NexGen Energy Ltd. and Mega Uranium Ltd., representing an aggregate of approximately 21.16% of the outstanding Anfield Shares and approximately 36.14% of the outstanding ISO Shares (on a non-diluted basis), have entered into voting support agreements, and have agreed, among other things, to vote their Anfield Shares and ISO Shares, respectively, in favour of the Transaction.

In addition to shareholder and court approvals, closing of the Transaction is subject to applicable regulatory approvals including, but not limited to, approval of the Toronto Stock Exchange (the “TSX”) and the TSX Venture Exchange (the “TSXV”) and the satisfaction of certain other closing conditions customary in transactions of this nature.

The Arrangement Agreement provides for customary deal protection provisions, including non-solicitation covenants of Anfield, “fiduciary out” provisions in favour of Anfield and “right-to-match superior proposals” provisions in favour of IsoEnergy. In addition, the Arrangement Agreement provides that, under certain circumstances, IsoEnergy would be entitled to a $5,000,000 termination fee. Each of IsoEnergy and Anfield have made customary representations and warranties and covenants in the Arrangement Agreement, including covenants regarding the conduct of their respective businesses prior to the closing of the Transaction.

Following completion of the Transaction, the ISO Shares will continue trading on the TSX and the Anfield Shares will be de-listed from the TSXV. Approximately 178.8 million ISO Shares are currently outstanding on a non-diluted basis and approximately 206.2 million ISO Shares are currently outstanding on a fully diluted basis. Upon completion of the Transaction (assuming no additional issuances of ISO Shares or Anfield Shares), there will be approximately 210.3 million ISO Shares outstanding on a non-diluted basis and approximately 251.5 million ISO Shares outstanding on a fully diluted basis.

IsoEnergy and Anfield will file material change reports in respect of the Transaction in compliance with Canadian securities laws, as well as copies of the Arrangement Agreement and the voting support agreements, which will be available under IsoEnergy’s and Anfield’s respective SEDAR+ profiles at www.sedarplus.ca.

Bridge Loan

In addition, in connection with the Transaction, IsoEnergy has provided a bridge loan in the form of a promissory note of approximately $6.0 million (the “Bridge Loan”) to Anfield, with an interest rate of 15% per annum and a maturity date of April 1, 2025, for purposes of satisfying working capital and other obligations of Anfield through to the closing of the Transaction. IsoEnergy has also agreed to provide an indemnity for up to US$3 million in principal (the “Indemnity”) with respect to certain of Anfield’s property obligations. The Bridge Loan and the Indemnity are secured by a security interest in all of the now existing and after acquired assets, property and undertaking of Anfield and guaranteed by certain subsidiaries of Anfield. The Bridge Loan, Indemnity and related security are subordinate to certain senior indebtedness of Anfield. The Bridge Loan is immediately repayable, among other circumstances, in the event that the Arrangement agreement is terminated by either IsoEnergy or Anfield for any reason.

Advisors

Canaccord Genuity Corp. is acting as financial advisor to IsoEnergy and has provided a fairness opinion to the IsoEnergy board of directors. Cassels Brock & Blackwell LLP is acting as legal advisor to IsoEnergy.

Haywood Securities Inc. is acting as financial advisor to Anfield and has provided a fairness opinion to the Anfield board of directors. DuMoulin Black LLP is acting as legal advisor to Anfield. Evans & Evans, Inc. has provided a fairness opinion to the Anfield special committee.

Conference Call / Webinar Details

IsoEnergy will host a conference call / webinar today at 12:00 p.m. Eastern Standard Time (“EST”) / 9:00 a.m. Pacific Standard Time (“PST”) to discuss the Transaction. Participants are advised to dial in five minutes prior to the scheduled start time of the call. A presentation will be made available on both IsoEnergy and Anfield’s websites prior to the conference call / webinar.

Webinar Details

Presenters: IsoEnergy CEO and Director, Philip Williams and COO, Marty Tunney

Date / Time: October 2, 2024 at 12:00 p.m. EST / 9:00 a.m. PST.

Webinar Access: Participants may join the webinar by registering using the link below.

https://event.choruscall.com/mediaframe/webcast.html?webcastid=qtgShXYz

Phone Access: Please use one of the following numbers.

Canada/US Toll Free

1-844-763-8274

International

1-412-717-9224

A recording of the conference call will be available on both company websites following the call.

Qualified Person Statement

The scientific and technical information contained in this news release with respect to IsoEnergy was reviewed and approved by Dean T. Wilton, PG, CPG, MAIG, a consultant of IsoEnergy, who is a “Qualified Person” (as defined NI 43-101).

The scientific and technical information contained in this news release with respect to Anfield was prepared Douglas L. Beahm, P.E., P.G., Anfield’s Chief Operating Officer, who is a “Qualified Person” (as defined NI 43-101).

About IsoEnergy

IsoEnergy Ltd. (TSX: ISO) (OTCQX: ISENF) is a leading, globally diversified uranium company with substantial current and historical mineral resources in top uranium mining jurisdictions of Canada, the U.S. and Australia at varying stages of development, providing near, medium, and long-term leverage to rising uranium prices. IsoEnergy is currently advancing its Larocque East Project in Canada’s Athabasca Basin, which is home to the Hurricane deposit, boasting the world’s highest grade Indicated uranium Mineral Resource.

IsoEnergy also holds a portfolio of permitted, past-producing conventional uranium and vanadium mines in Utah with a toll milling arrangement in place with Energy Fuels Inc. These mines are currently on stand-by, ready for rapid restart as market conditions permit, positioning IsoEnergy as a near-term uranium producer.

About Anfield

Anfield is a uranium and vanadium development and near-term production company that is committed to becoming a top-tier energy-related fuels supplier by creating value through sustainable, efficient growth in its assets. Anfield is a publicly traded corporation listed on the TSX-Venture Exchange (AEC-V), the OTCQB Marketplace (ANLDF) and the Frankfurt Stock Exchange (0AD).

Further Information & Investor Relations Inquiries

IsoEnergy Ltd.

Philip Williams

CEO and Director

Email: info@isoenergy.ca

Phone: 1-833-572-2333

Website: www.isoenergy.ca

Anfield Energy Inc.

Corey Dias

CEO and Director

Email: contact@anfieldenergy.com

Phone: 780-920-5044

Website: https://anfieldenergy.com/

In Europe:

Swiss Resource Capital AG

Jochen Staiger & Marc Ollinger

info@resource-capital.ch

www.resource-capital.ch

Neither the TSXV nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this news release. No securities regulatory authority has either approved or disapproved of the contents of this news release.

None of the securities to be issued pursuant to the Arrangement have been or will be registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act”), or any state securities laws, and any securities issuable in the Arrangement are anticipated to be issued in reliance upon available exemptions from such registration requirements pursuant to Section 3(a)(10) of the U.S. Securities Act and applicable exemptions under state securities laws. This press release does not constitute an offer to sell, or the solicitation of an offer to buy, any securities.

Cautionary Statement Regarding Forward-Looking Information

This press release contains “forward-looking information” within the meaning of applicable Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved”. These forward-looking statements or information may relate to the Transaction, including statements with respect to the consummation and timing of the Transaction; receipt and timing of approval of Anfield’s shareholders with respect to the Transaction; receipt and timing of approval of IsoEnergy’s shareholders with respect to the Transaction; the anticipated benefits of the Transaction to the parties and their respective shareholders; the expected receipt of court, regulatory and other consents and approvals relating to the Transaction; the expected ownership interest of IsoEnergy shareholders and Anfield shareholders in the combined company; the expected production capacity of the combined company; anticipated strategic and growth opportunities for the combined company; the successful integration of the businesses of IsoEnergy and Anfield; the prospects of each companies’ respective projects, including mineral resources estimates and mineralization of each project; the potential for, success of and anticipated timing of commencement of future commercial production at the companies’ properties, including expectations with respect to any permitting, development or other work that may be required to bring any of the projects into development or production; increased demand for nuclear power and uranium and the expected impact on the price of uranium; and any other activities, events or developments that the companies expect or anticipate will or may occur in the future.

Forward-looking statements are necessarily based upon a number of assumptions that, while considered reasonable by management at the time, are inherently subject to business, market and economic risks, uncertainties and contingencies that may cause actual results, performance or achievements to be materially different from those expressed or implied by forward-looking statements. Such assumptions include, but are not limited to, assumptions that IsoEnergy and Anfield will complete the Transaction in accordance with, and on the timeline contemplated by the terms and conditions of the relevant agreements; that the parties will receive the required shareholder, regulatory, court and stock exchange approvals and will satisfy, in a timely manner, the other conditions to the closing of the Transaction; the accuracy of management’s assessment of the effects of the successful completion of the Transaction and that the anticipated benefits of the Transaction will be realized; the anticipated mineralization of IsoEnergy’s and Anfield’s projects being consistent with expectations and the potential benefits from such projects and any upside from such projects; the price of uranium; that general business and economic conditions will not change in a materially adverse manner; that financing will be available if and when needed and on reasonable terms; and that third party contractors, equipment and supplies and governmental and other approvals required to conduct the combined company’s planned activities will be available on reasonable terms and in a timely manner. Although each of IsoEnergy and Anfield have attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking information.

Such statements represent the current views of IsoEnergy and Anfield with respect to future events and are necessarily based upon a number of assumptions and estimates that, while considered reasonable by IsoEnergy and Anfield, are inherently subject to significant business, economic, competitive, political and social risks, contingencies and uncertainties. Risks and uncertainties include, but are not limited to the following: the inability of IsoEnergy and Anfield to complete the Transaction; a material adverse change in the timing of and the terms and conditions upon which the Transaction is completed; the inability to satisfy or waive all conditions to closing the Transaction; the failure to obtain shareholder, regulatory, court or stock exchange approvals in connection with the Transaction; the inability of the combined company to realize the benefits anticipated from the Transaction and the timing to realize such benefits; the inability of the consolidated entity to realize the benefits anticipated from the Arrangement and the timing to realize such benefits, including the exploration and drilling targets described herein; unanticipated changes in market price for ISO Shares and/or Anfield Shares; changes to IsoEnergy’s and/or Anfield’s current and future business plans and the strategic alternatives available thereto; growth prospects and outlook of Anfield’s business; regulatory determinations and delays; stock market conditions generally; demand, supply and pricing for uranium; and general economic and political conditions in Canada, the United States and other jurisdictions where the applicable party conducts business. Other factors which could materially affect such forward-looking information are described in the risk factors in each of IsoEnergy’s and Anfield’s most recent annual management’s discussion and analyses or annual information forms and IsoEnergy’s and Anfield’s other filings with the Canadian securities regulators which are available, respectively, on each company’s profile on SEDAR+ at www.sedarplus.ca. IsoEnergy and Anfield do not undertake to update any forward-looking information, except in accordance with applicable securities laws.

Disclaimer on Mineral Resource Estimates

Each of the mineral resource estimates of IsoEnergy and Anfield, except for the Larocque East Project, Tony M Mine and Velvet-Wood/Slick Rock Project, contained in this press release are considered to be “historical estimates” as defined under NI 43-101. A Qualified Person has not done sufficient work to classify the historical estimates as current mineral resources or mineral reserves and IsoEnergy and Anfield are not treating the historical estimates as current mineral resources or mineral reserves.

For additional information regarding IsoEnergy’s Tony M mine, including the mineral resource estimate, please refer to the Technical Report entitled “Technical Report on the Tony M Mine, Utah, USA – Report for NI 43-101” dated effective September 9, 2022 prepared by SLR Consulting (Canada) Ltd., available under IsoEnergy’s profile on www.sedarplus.ca. The “qualified person” for this technical report is Mark B. Mathisen, C.P.G., Principal Geologist, SLR Consulting International Corp. Mr. Mathisen is a “qualified person” under NI 43-101.

For additional information regarding Anfield’s Velvet-Wood and Slick Rock projects and the Shootaring Canyon Mill, including the mineral resource estimates, please refer to the Technical Report entitled “The Shootaring Canyon Mill and Velvet-Wood and Slick Rock Uranium Projects, Preliminary Economic Assessment, National Instrument 43-101” dated effective May 6, 2023 (the “Velvet-Wood/Slick Rock PEA”), available under Anfield’s profile on www.sedarplus.ca. The technical report was prepared by Douglas L. Beahm, P.E., P.G., Harold H. Hutson, P.E., P.G., Carl D. Warren, P.E., P.G. and Terrence (Terry) McNulty, P.E., D. Sc. T.P., each of whom is a “qualified person” under NI 43-101.

Disclaimer on Historical Mineral Resource Estimates

Daneros Mine: Reported by Energy Fuels Inc. in a technical report entitled “Updated Report on the Daneros Mine Project, San Juan County, Utah, U.S.A.”, prepared by Douglas C. Peters, C. P. G., of Peters Geosciences, dated March 2, 2018.

Sage Plain Project: Reported by Energy Fuels Inc. in a technical report entitled “Updated Technical Report on Sage Plain Project (Including the Calliham Mine)”, prepared by Douglas C. Peters, CPG of Peters Geosciences, dated March 18, 2015.

Coles Hill: reported by Virginia Uranium Holdings Inc. In a technical report entitled “NI43-101 preliminary economic assessment update (revised)”, prepared by John I Kyle of Lyntek Incorporated, dated august 19, 2013.

In each instance, the historical estimate is reported using the categories of mineral resources and mineral reserves as defined by the Canadian Institute CIM Definition Standards for Mineral Reserves, and mineral reserves at that time, and these “historical estimates” are not considered by IsoEnergy to be current. In each instance, the reliability of the historical estimate is considered reasonable, but a Qualified Person has not done sufficient work to classify the historical estimate as a current mineral resource, and IsoEnergy is not treating the historical estimate as a current mineral resource. The historical information provides an indication of the exploration potential of the properties but may not be representative of expected results.

For the Daneros Mine, as disclosed in the above noted technical report, the historical estimate was prepared by Energy Fuels using a wireframe model of the mineralized zone based on an outside bound of a 0.05% eu3o8 grade cutoff at a minimum thickness of 1 foot. Surface drilling would need to be conducted to confirm resources and connectivity of resources in order to verify the Daneros historical estimate as a current mineral resource.

For the Sage Plain Project, as disclosed in the above noted technical report, the historical estimate was prepared by Peters Geosciences using a modified polygonal method. An exploration program would need to be conducted, including twinning of historical drill holes, in order to verify the Sage Plain historical estimate as a current mineral resource.

For the Coles Hill Project, as disclosed in the above noted revised preliminary economic assessment, the historical estimated was prepared by John I Kyle of Lyntek Incorporated. Twinning of a selection of certain holes would need to be completed along with updating of mining, processing and certain cost estimates in order to verify the Coles Hill Project historical resource estimate as a current mineral resource estimate.

Marquez-Juan Tafoya: reported by enCore Energy Corporation in a technical report entitled “Marquez-Juan Tafoya Uranium Project, 43-101 Technical Report, Preliminary Economic Assessment” dated effective June 9, 2021, prepared by Douglas L. Beahm, P.E., P.G. and Terrence (Terry) McNulty, P.E., D. Sc. T.P.

Frank M: reported by Uranium One Americas in a technical report entitled ”Findlay Tank SE Breccia Pipe Uranium Project, Mohave County, Arizona, USA, 43-101 Mineral Resource Report” dated October 2, 2008 prepared by Douglas L. Beahm, P.E., P.G. of BRS Inc.

West Slope: reported by Anfield Energy Inc. in a technical report entitled “US DOE Uranium/Vanadium Leases JD-6, JD-7, JD-8, and JD-9, Montrose County, Colorado, USA, Mineral Resource Technical Report, National Instrument 43-101” dated effective April 10, 2022, prepared by Douglas L. Beahm, P.E., P.G., and Joshua Stewart, PE. P.G. of BRS Inc.

Findlay Tank: reported by Uranium One Americas in a technical report entitled ”Frank M Uranium Project, 43-101 Mineral Resource Report, Garfield County, Utah USA” dated June 10, 2008 prepared by Douglas L. Beahm, P.E., P.G. and Andrew C. Anderson, P.E., P.G., of BRS Inc.

Artillery Peak/Date Creek: reported by Anfield Energy Inc. in a technical report entitled “Artillery Peak Exploration Project, Mohave County, Arizona, 43-101 Technical Report” dated effective October 12, 2010, prepared by Dr. Karen Wenrich.

[1] For additional information, see the Tony M Technical Report and Velvet-Wood/Slick Rock PEA.

[2] This estimate is a “historical estimate” as defined under NI 43-101. A Qualified Person has not done sufficient work to classify the historical estimate as current mineral resources and neither IsoEnergy nor Anfield is treating the historical estimate as current mineral resources. See Appendix for additional details.

[3] Each of the mineral resource estimates of IsoEnergy and Anfield, except for the Tony M Mine and Velvet-Wood/Slick Rock Project, contained in this press release are considered to be “historical estimates” as defined under National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”). A Qualified Person has not done sufficient work to classify the historical estimates as current mineral resources or mineral reserves and IsoEnergy and Anfield are not treating the historical estimates as current mineral resources or mineral reserves. See Disclaimer on Mineral Resource Estimates below for additional details.

Swiss Resource Capital AG

Poststrasse 1

CH9100 Herisau

Telefon: +41 (71) 354-8501

Telefax: +41 (71) 560-4271

http://www.resource-capital.ch

CEO

Telefon: +41 (71) 3548501

E-Mail: js@resource-capital.ch

![]()